Navigating high-beta digital asset equities like MARA (Marathon Digital) or CONL (2x Long Coinbase Daily ETF) requires more than a standard directional bias. These instruments operate within a regime of severe volatility clustering—extended periods of grinding consolidation punctuated by violent, exponential expansions or drawdowns.

For thematic tech investors holding concentrated allocations in these vehicles, standard “Buy and Hold” often leads to severe psychological and capital drawdowns. To survive and compound capital, one must deploy a institutional framework combining mathematical rebalancing and strategic options underwriting.

Here is the playbook for managing high-beta crypto equity risk, protecting your capital runway, and optimizing for structural tax alpha.

1. The Break-Even Architecture: The Mathematics of Drawdowns

The psychological urge to “hold until break-even” often masks a dangerous mathematical reality. In leveraged or high-beta instruments, volatility drag and asymmetric variance can permanently impair capital.

Look at the underlying math of recovery:

- A 20% drawdown requires a 25% return just to break even.

- A 50% drawdown requires a 100% return to recover your principal.

- An 80% drawdown requires an astronomical 400% return to get back to par.

If a position like CONL or MARA constitutes over 30% of your total portfolio equity, you are exposed to catastrophic tail risk. The institutional response is not to pray for a market reversal, but to implement a Vol-Adjusted Rebalancing Protocol.

When the underlying asset spikes into overbought territory (based on 14-day RSI > 70 or upper Bollinger Band extensions), you must methodically liquidate a portion of the high-beta position, rotating the proceeds into cash equivalents or low-beta yield vehicles. This cash becomes your dry powder to re-enter when volatilityMean-reverts.

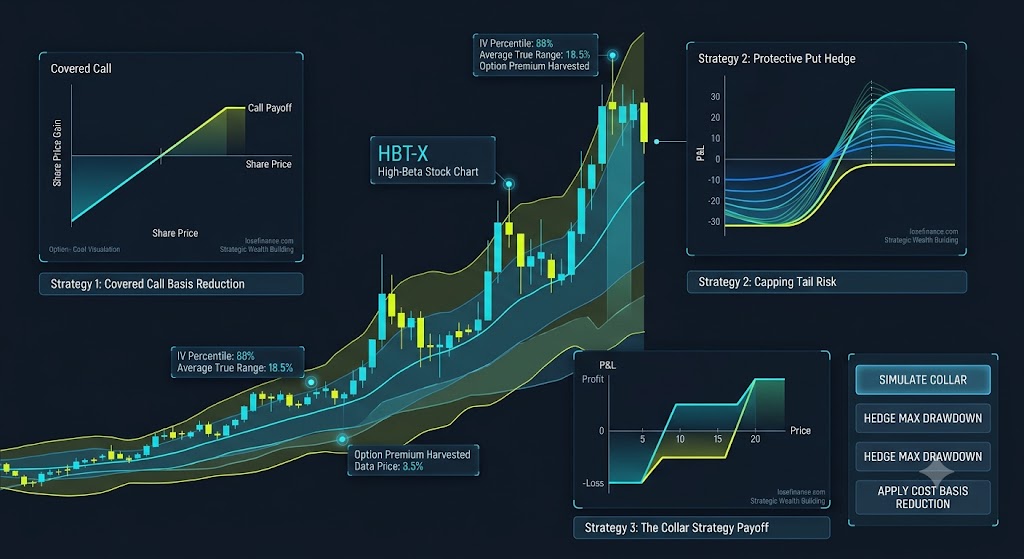

2. Compressing Cost-Basis via Synthetic Covered Calls

If your objective is to liquidate a legacy position as close to your break-even point as possible, sitting dormant is a sub-optimal strategy. You should actively put your equity to work by underwriting volatility.

By utilizing the elevated Implied Volatility (IV) inherent to crypto equities, you can execute a Covered Call Framework:

[Buy/Hold Underlying Equity] + [Sell Out-of-the-Money (OTM) Call Options]

The Execution Model

- Delta Selection: Sell Calls with a 0.20 to 0.25 Delta, expiring 30 to 45 days out. This gives you a high statistical probability of the option expiring worthless while capturing rich premium.

- Strike Alignment: Align the strike price exactly with your technical resistance zones or your calculated break-even target.

- The Outcome: The premium collected instantly compresses your net cost-basis. If the stock trends sideways or down slightly, the premium offsets the loss. If the stock gaps up violently and passes your strike, your shares are called away at your target price, securing your planned exit cleanly.

3. Advanced Tax Alpha: Navigating Digital Asset Tax Traps

Active rebalancing and options underwriting generate phenomenal cash flow, but they trigger a dangerous secondary bottleneck: Short-Term Capital Gains Taxes. In jurisdictions like the United States, short-term gains are taxed at ordinary income rates, heavily cannibalizing your portfolio’s compounding efficiency.

To capture true “Tax Alpha,” institutional traders deploy three specific structural frameworks:

Vector A: Constructive Sales and Option Straddles

If you have massive unrealized gains in a stock like MARA but want to lock in lock in protection without triggering a taxable disposal event, directly selling the shares is a taxable trigger. Instead, institutional desks utilize deep in-the-money puts or synthetic short positions to freeze the equity risk while legally deferring the capital gains realization into the next fiscal tax year.

Vector B: The Wash-Sale Rule Arbitrage

If you are underwater on a crypto equity and want to harvest the capital loss to offset other gains, remember the Wash-Sale Rule. You cannot sell MARA for a loss and buy it back within 30 days. However, you can harvest the loss on the equity and immediately sell deep in-the-money cash-secured puts or rotate into a highly correlated alternative asset class, keeping your structural sector exposure alive while banking the tax deduction.

Vector C: Structural Wrapper Optimization (Section 1256 Contracts)

Whenever possible, instead of trading single-stock equities which trigger standard equity tax regimes, consider allocating a portion of your risk capital to standardized index options (like SPX or NDX derivatives) or cash-settled crypto futures options. These fall under Section 1256 Contracts, which enjoy a highly favorable 60/40 tax treatment (60% long-term capital gains, 40% short-term capital gains), regardless of how short the holding period was.

The Tactical Summary

High-beta crypto equities are magnificent vehicles for expanding alpha, but they are unforgiving to structural negligence. Do not let your portfolio be held hostage by emotional attachment to a entry price.

Deploy systematic covered calls to lower your break-even horizon, hedge tail risk with mathematically sound sizing, and always consult a certified tax professional to ensure your options premiums and rebalancing events are structured to minimize fiscal drag.

Related Institutional Frameworks:

- Need a foundational baseline? Read our guide on The Macro-Technology Nexus to understand how liquidity cycles dictate market entry.

- New to derivatives? Explore our Options Playbook for a deep dive into premium harvesting and volatility management.

- Confused by the fine print? Ensure you are fully aligned with our Legal Disclaimer before implementing these strategies.

Disclaimer: The information provided in this article is for informational, educational, and structural analysis purposes only and does not constitute official tax, legal, or financial advice. Crypto-linked equities, leveraged ETFs, and derivatives carry extreme financial risk. Always consult a Certified Public Accountant (CPA) or licensed financial advisor regarding your specific tax jurisdiction and risk profile.

Leave a Reply